European Accelerator Report 2016

#EuropeanAcceleratorReport

Introduction

Over the last few years, accelerators and the programs they operate have become key players

within startup ecosystems, helping thousands of founders build and grow innovative businesses

in today's "new economy." Accelerators have become far more than simple business-service

providers or investment vehicles, instead emerging as invaluable operators within public and

private spheres. They bring together entrepreneurs, investors, public entities, and

corporations with the common goal of helping innovative businesses quickly take root.

Policymakers and other actors in the startup community should understand the essential role of

accelerators within the startup ecosystem, as proper incentivization of accelerators has the potential to

effectively facilitate the cultivation and cross-pollination of startups.

The European Accelerator Report 2016 provides an exclusive inside look

at accelerator programs in the region.

This report is a follow-up on the

2015 Accelerator Report

and aims to explain how the accelerator industry is evolving in the region,

how accelerators support their activities, and how they impact local and regional

tech startup ecosystems.

Please note that many organizations supporting entrepreneurship, such as incubators and

venture builders, have not been included in the scope of this report, even if they share

some common traits with accelerators.

Accelerator — an evolving definition:

The acceleration industry is evolving rapidly, and it is becoming increasingly

difficult to precisely define what an accelerator is. As new models emerge,

the term "accelerator" describes an increasingly diverse set of programs and organizations, and,

often, the lines that distinguish accelerators from similar institutions, like incubators and

early-stage funds, become blurred. For the purposes of this report, accelerators can be

defined according to Miller and Bound (2011), and share these common traits:

1) An application process that is open to all, yet highly competitive.

2) Possible provision of pre-seed investment (grant or equity).

3) A focus on small teams instead of individual founders.

4) Time-limited support comprising programmed events and intensive mentoring.

5) Cohorts or ‘classes’ of startups rather than individual companies.

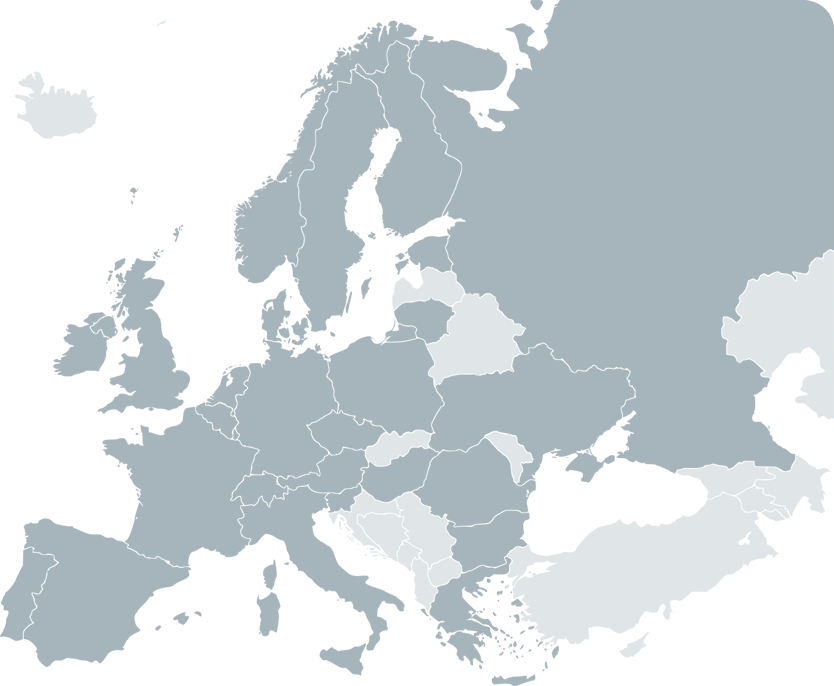

Total investment in the region

€47,575,976

in 3,701 startups

by 193 accelerator programs

-

United Kingdom

-

€15,566,629 invested in 992 startups from 44 accelerators

-

Most cash invested:

500 Startups

Most startups accelerated:

MassChallenge

-

France

-

€2,000,001 invested in 612 startups from 23 accelerators

-

Most cash invested:

Numa Paris

Most startups accelerated:

Impulse Labs

-

Spain

-

€7,458,380 invested in 428 startups from 26 accelerators

-

Most cash invested:

IMPACT Accelerator

Most startups accelerated:

Conector Startup Accelerator

-

Germany

-

€6,431,085 invested in 218 startups from 17 accelerators

-

Most cash invested:

Techstars

Most startups accelerated:

TechFounders

-

Portugal

-

€220,000 invested in 180 startups from 5 accelerators

-

Most cash invested:

Building Global Innovators - BGI

Most startups accelerated:

Beta-i

-

Netherlands

-

€1,855,000 invested in 169 startups from 8 accelerators

-

Most cash invested:

Rockstart

Most startups accelerated:

HighTechXL Accelerator

-

Italy

-

€2,780,000 invested in 158 startups from 10 accelerators

-

Most cash invested:

TIM #WCAP Accelerator

Most startups accelerated:

IHM

-

Switzerland

-

€1,675,000 invested in 138 startups from 6 accelerators

-

Most cash invested:

Kickstart Accelerator

Most startups accelerated:

MassChallenge Switzerland

-

Austria

-

€892,000 invested in 124 startups from 4 accelerators

-

Most cash invested:

Impact Hub Vienna

Most startups accelerated:

Impact Hub Vienna

-

Ukraine

-

€0 invested in 100 startups from 1 accelerator

-

Most cash invested:

-

Most startups accelerated:

GrowthUP

-

Finland

-

€60,000 invested in 97 startups from 6 accelerators

-

Most cash invested:

KIUAS Accelerator

Most startups accelerated:

Startup Sauna

-

Denmark

-

€1,539,797 invested in 85 startups from 2 accelerators

-

Most cash invested:

Accelerace

Most startups accelerated:

Accelerace

-

Sweden

-

€696,901 invested in 61 startups from 6 accelerators

-

Most cash invested:

500 Startups

Most startups accelerated:

STING (Stockholm Innovation & Growth)

-

Norway

-

€100,000 invested in 60 startups from 3 accelerators

-

Most cash invested:

FintechFactory

Most startups accelerated:

StartupLab

-

Belgium

-

€225,000 invested in 60 startups from 7 accelerators

-

Most cash invested:

Roularta Mediatech Accelerator

Most startups accelerated:

LeanSquare

-

Poland

-

€80,000 invested in 49 startups from 5 accelerators

-

Most cash invested:

GammaRebels

Most startups accelerated:

MIT Enterprise Forum Poland

-

Ireland

-

€1,130,000 invested in 36 startups from 1 accelerator

-

Most cash invested:

NDRC

Most startups accelerated:

NDRC

-

Slovenia

-

€450,000 invested in 31 startups from 2 accelerators

-

Most cash invested:

ABC Accelerator

Most startups accelerated:

ABC Accelerator

-

Czech Republic

-

€450,000 invested in 23 startups from 2 accelerators

-

Most cash invested:

StartupYard

Most startups accelerated:

StartupYard

-

Estonia

-

€440,000 invested in 20 startups from 2 accelerators

-

Most cash invested:

Startup Wise Guys

Most startups accelerated:

Startup Wise Guys

-

Bulgaria

-

€70,000 invested in 15 startups from 3 accelerators

-

Most cash invested:

Segments Accelerator

Most startups accelerated:

Eleven Ventures

-

Luxembourg

-

€0 invested in 12 startups from 1 accelerator

-

Most cash invested:

-

Most startups accelerated:

Paul Wurth InCub

-

Hungary

-

€368,000 invested in 10 startups from 2 accelerators

-

Most cash invested:

Aquincum Incubator

Most startups accelerated:

Aquincum Incubator

-

Russia

-

€89,600 invested in 8 startups from 1 accelerator

-

Most cash invested:

Numa Moscow

Most startups accelerated:

Numa Moscow

-

Lithuania

-

€200,000 invested in 7 startups from 2 accelerators

-

Most cash invested:

Blue Lime Labs

Most startups accelerated:

Blue Lime Labs

-

Romania

-

€100,000 invested in 7 startups from 1 accelerator

-

Most cash invested:

Risky Business

Most startups accelerated:

Risky Business

-

Greece

-

€25,000 invested in 1 startups from 1 accelerator

-

Most cash invested:

The Accelerator - by Metavallon

Most startups accelerated:

The Accelerator - by Metavallon

-

Top 10 countries by investment

-

United Kingdom

€15,566,629

-

Spain

€7,458,380

-

Germany

€6,431,085

-

Italy

€2,780,000

-

France

€2,000,001

-

Netherlands

€1,855,000

-

Switzerland

€1,675,000

-

Denmark

€1,539,797

-

Ireland

€1,130,000

-

Austria

€892,000

-

-

Top 10 countries by startups accelerated

-

United Kingdom

992

-

France

612

-

Spain

428

-

Germany

218

-

Portugal

180

-

Netherlands

169

-

Italy

158

-

Switzerland

138

-

Austria

124

-

Ukraine

100

-

52 Exits reported by 24 accelerators in 2016

⬆ 37% more than 2015

TOP 10 SEED ACCELERATORS

By capital invested

-

Techstars

€5,807,941

Europe | Private fund

-

IMPACT

€4,030,000

Spain | Mix fund

-

500 Startups

€3,819,765

Europe | Private fund

-

Wayra

€2,410,000

Europe | Private fund

-

Collider

€1,610,943

United Kingdom | Private fund

-

Accelerace

€1,539,797

Denmark | Mix fund

-

Startupbootcamp

€1,200,000

Europe | Mix fund

-

BioCity Accelerator

€1,167,350

United Kingdom | Private fund

-

L Marks

€1,167,350

United Kingdom | Private fund

-

NDRC

€1,130,000

Ireland | Public fund

Top seed accelerators ranked by cash amount invested into startups (excludes provided services, mentorship, coworking space, or follow-up investment).

This ranking is not a measure of the success or quality of these programs.

TYPE OF ORGANIZATION

Are you a for-profit organization?

- For-profit

- Not-for-profit

66.3% of accelerators in the region claim to be for-profit ventures, similar to what was reported in the 2015 edition (64.6%). Typically, for-profit accelerators are funded with private capital from investors aiming to generate long-term profit. This is primarily accomplished by the appreciation of their equity in startups, but also by providing business-support services and by offering “acceleration-as-a-service” to large corporations.

Not-for-profit accelerators support industries that provide a specific public benefit, such as Healthtech and Edtech. Others aim to boost entrepreneurship in their communities. They may also focus on providing new opportunities for minority groups or look to boost economic activity in a given region. These programs and the organizations operating them may be either privately or publicly funded. Generally, these programs do not take equity and instead offer free support.

Examples of not-for-profit accelerators include Startup Sauna, SeedRocket, MassChallenge, and Fast Track Malmö.

SOURCES OF ACCELERATOR FUNDING

How are you funded?

- Private funding only

- Mix of both (Public/Private)

- Public funding only

-

57.9% of accelerators in Europe are completely funded by private capital. Investors include high net worth individuals, angel groups, private investors (i.e. venture capital investment funds), and/or corporations. They seek to profit through positive startup exits (acquisitions, IPOs, etc.) and by having early access to high-potential tech companies.

35.8% of accelerator programs operating in the region have received a mix of public and private funding, showing high levels of cooperation between public and private organizations.

THE ACCELERATOR BUSINESS MODEL

What was your main source of revenue in 2016?

-

Corporate sponsorship

32%

-

Corporate partnerships (operating acceleration program w/corporation)

23%

-

No revenue

16%

-

Charge for mentorship

8%

-

Other

8%

-

Exit of startups

6%

-

Charge for office space

5%

-

Events

3%

How will you generate revenue in the medium & long terms?

-

Corporate partnerships (operating acceleration program w/corporation)

45%

-

Corporate sponsorship

44%

-

Exit of startups

32%

-

Other

18%

-

Charge for mentorship

18%

-

Charge for office space

13%

-

Events

11%

In the 2015 Report, 60.2% accelerators indicated that they intended to

follow the traditional "cash-for-equity" model, first established in 2005 by Y

Combinator, which involves investing a small amount of seed money in a startup

— around $25,000 on average — in exchange for equity (usually between 5% and 10%).

Increasingly, this model is becoming rare as accelerators reconsider their general outlook.

Most likely, the small number of exits — 52 reported in 2016 — has proven insufficient

in funding their operations.

Only 6% of accelerators operating in the region reported

exits as a main source of revenue in 2016.

53.2% of accelerators take equity in startups and

32% predict making revenue from exits in the future.

Accelerators have historically relied on, and continue to explore, alternative models of revenue generation.

90% plan to increase their revenue in the medium- to long-term by

incorporating such models, including, but not limited to, charging

for mentorship, subletting office space, hosting events, and working with corporations.

As we predicted last year, the relationships between accelerators and

corporations have grown stronger and more numerous.

53.7% of accelerators are at least partially funded by a corporation, and

66.8% aim to generate future revenue from services sold to corporations.

Corporate revenue generated by accelerators came from two main sources in 2016:

23% was a result of corporate partnerships, generally in the form of a white-labeled

or jointly-run acceleration program created by the accelerator on behalf of the corporation, and

32% came from corporate sponsorship packages sold by accelerators.

EUROPEAN ACCELERATOR EQUITY AND INVESTMENT MODEL

Do you invest cash?

- Cash investment

- No investment

Accelerators that do not invest cash generally focus on providing services and resources such as workshops, mentorships, coworking spaces and connections.

Do you take equity from participating companies?

- Yes

- No

What range?

-

Equity free

47%

-

Between 1% and 3%

7%

-

Between 4% and 6%

16%

-

Between 7% and 10%

21%

-

Over 10%

4%

-

Undisclosed

5%

MAIN TRENDS

In 2016, the acceleration model has continued to grow and evolve. Four major trends can be identified.

Trend 1: Growing ties between accelerators & corporations

Corporate funding

- Corporate funding

- Non-corporate funding

“Corporations are increasingly engaging in a more meaningful way with startup founders and the broader entrepreneurial ecosystem,” said Bobby Franklin, President and CEO of NVCA. The number of venture capital firms (VCs) has grown by 15.5% each year between 2011 and 2015, according to data from CB Insights. This growth in corporate engagement in the startup ecosystem is beginning to spill over into the accelerator industry.

Corporate revenue in 2017

- Corporate revenue

- Non-corporate revenue

As the accelerator industry matures, we are seeing increased collaboration between accelerators and corporations. “On the one hand, this is because corporations are discovering that accelerators are an efficient and effective way to engage with startups. On the other hand, accelerators understand that corporations can help them fund operations in the short-to-medium term (exits are often far out). They improve the prospects of their portfolio companies that can potentially sell to, raise funds from, or be acquired by these corporations," said Miklos Grof, co-author of this report.

There is a growing trend for corporations to outsource their acceleration programs due to their limited skills in accelerating startups. Some voices in the startup ecosystem, notably high-profile venture capitalist Fred Wilson, welcome this development. He believes, “Corporations should BUY companies. Investing in companies makes no sense,” as cited by CB Insights.

Corporations can benefit from accelerators in 5 different ways:

- Launching a program quickly and cost-effectively: by partnering with accelerators, corporations can quickly enter the acceleration business and adopt best practices developed by accelerators over years of operation.

- Enhancing deal flow: by accessing the accelerator’s immense marketing power and network.

- Staying up to date: by having access to an accelerator’s deal flow, they receive insight into the innovation pipeline in their market. Corporations have learned that competitors now often come from the startup world.

- Building an innovative corporate culture: by placing their corporate executives as mentors in the accelerator or by enabling their own corporate executives to innovate. In the latter case, the new product could be placed into a separate company that is then accelerated by the accelerator.

- Building a more innovative brand: by aligning with accelerators and their startups which have become symbols of innovation in the eyes of the public.

Examples of accelerators that are aligning themselves with corporations include: 33ENTREPRENEURS, Collider, Conector Startup Accelerator, and L Marks.

Trend 2: Verticalization

Are your program(s) focused on specific verticals?

- Yes

- No

Accelerator verticalization is driven in part by the following:

- Establishing core competence: accelerators have realized that it is hard to attract and choose high potential startups when they are 'jack-of-all-trades'.

- Responding to corporate clients: the expertise of a corporate sponsor or partner is confined to the industry in which it operates.

- Brand building: in order to offer more "concentrated" value to startups and attract the best founders, accelerators need to position themselves in their ecosystems and attract more experienced mentors and investors.

Continuing the trend identified in the 2015 report, the acceleration landscape in the region is increasingly moving towards verticalization, with 62.6% of accelerators running programs focused on a particular industry or sector niche. This trend is likely to continue as regional startup ecosystems continue to mature. This is a very positive development because verticalized accelerators generally bring more value to startups through more qualified acceleration teams, larger pools of quality mentors within the industry, and close corporate ties to related markets.

Some examples of verticalized accelerators in the region include: Startupbootcamp Fintech, Merck Accelerator, Emerge Education, and Next Media Accelerator.

Trend 3: Expansion

Do you plan to expand to new locations in 2017?

After reaching a certain level of maturity, expansion becomes a natural next step for well-established accelerators. This growth comes in three forms: by opening new vertical programs, by launching new programs in different cities, or by launching programs internationally. Some examples include the recent international launch of programs run by European accelerators, such as Startupbootcamp and NUMA in Mexico or Rockstart in Colombia.

According to Sebastien Brunet, co-author of this report, “There are different reasons for which an accelerator decides to go abroad: to help their startup portfolios expand to new markets by providing softlanding services, to source innovative startups from new regions, to increase the quality of their deal flow and to reinforce their brands on an international level.”

International expansion usually happens in two ways:

- By merging or acquiring an already existing accelerator in a new country.

- By partnering with a local player, for example a VC fund.

Trend 4: Blurring lines

Traditionally, the norm for an accelerator was to accelerate 10-30 startups per year by investing $20,000-$50,000 in each business.

Today, accelerators often operate across the investment life cycle in an attempt to fill the gaps in local startup ecosystems and cater to potential financial partners and sponsors. These include governments, universities, and corporations. New operating models have evolved immensly, thereby blurring the lines between accelerators, incubators, and early-stage funds. Of the 193 accelerator programs included in this report, 30% described themselves as a combined accelerator, incubator, venture capital fund, and/or angel group.

TOP 20 ACTIVE ACCELERATORS

By number of startups accelerated in 2016

-

-

Country

-

Accelerator

-

Startups accelerated in 2016

-

-

-

-

MassChallenge Europe

-

170

-

-

-

-

EIT Digital Accelerator

-

130

-

-

-

-

Impulse Labs

-

127

-

-

-

-

GrowthUP

-

100

-

-

-

-

Impact Hub Vienna

-

97

-

-

-

-

Beta-i

-

92

-

-

-

-

Conector

-

88

-

-

-

-

Startupbootcamp Europe

-

80

-

-

-

-

BioCity Accelerator

-

80

-

-

-

-

P.Factory

-

70

-

-

-

-

Female Founders Accelerator

-

67

-

-

-

-

Fábrica de Startups

-

66

-

-

-

-

Accelerace

-

65

-

-

-

-

HighTechXL Accelerator

-

60

-

-

-

-

Euratechnologies

-

58

-

-

-

-

BoostInLyon

-

55

-

-

-

-

Starburst

-

55

-

-

-

-

Lanzadera

-

54

-

-

-

-

IMPACT Accelerator

-

52

-

-

-

-

Techstars

-

51

-

This ranking is not a measure of the success or quality of these programs.

HOT MARKETS

in the region in 2016

% of accelerators that reported an interest in investing in these markets in the next 12 months

-

Internet of things

60.5%

-

Big data analytics

54.7%

-

Saas

53.7%

-

Fintech

49.5%

-

Health

45.8%

-

Cloud services

37.4%

-

Wearables

35.3%

-

Mobile apps

34.7%

-

Others

34.2%

-

Cleantech

33.2%

-

E-commerce

33.2%

-

Agritech

28.9%

-

Drones

28.9%

-

Biotech

23.7%

-

Adtech

23.2%

-

Education

22.1%

-

Social media analytics

20.0%

-

Real estate

14.2%

THE LOCAL INSIGHT

How do you see the accelerator model changing /evolving in Europe in the next couple of years?

-

-

Rune Theill

Rockstart Accelerator (Netherlands)

The dramatic increase in accelerators have made our founders' needs different from when we first started 5 years ago. We find ourselves evolving when their needs evolve. For instance, over the years, we've made sure that we've developed specialization in having the right investor and industry mentor contacts for our startups to have a leg up in accessing the right customers, research, and key industry decision-makers. Accelerator specialization is going to be increasingly important in Europe, and is going to be a key factor continuing to support European entrepreneurs moving forward.

-

-

Nacho de Pinedo

IMPACT Accelerator (Spain)

The accelerator sector is growing and being professionalized. The community has grown from very few accelerators offering only informal services to more than 400 accelerators covering a wide range of niches and verticals. We expect to see more niche accelerators, regarding the services provided and the verticals covered. We also expect to see more big corporations relying on professional accelerators to help with innovation, technology and investment challenges.

-

-

-

Rishi Chowdhury

IncuBus Ventures & Momentum London (United Kingdom)

The accelerator space is rapidly shifting. More and more programmes are entering the market and choosing niche focuses. However I see the biggest change being a shift away from the funding / equity model to a more sustainable model for the long term success of an accelerator programme. We hope to be leading the way with that with the Momentum London programme.

-

-

Jill Lindström

STING (Sweden)

In Stockholm, we see a clear increase in the verticalization of startup support and hubs. This provides entrepreneurs with much more sector-specific know-how and networks than the more general accelerators have done in the past. I believe this development will continue, especially as more corporations are starting their own accelerators in an effort to get access to innovative products and services within their industries

-

THE REPORT

-

427

Institutions contacted

80% more than 2015

-

224

Replies

60% more than 2015

-

156

Accelerators

37% more than 2015

-

27

Countries

3 more than 2015

Accelerator programs by country

-

United Kingdom

44

-

Spain

26

-

France

23

-

Germany

17

-

Italy

10

-

Netherlands

8

-

Belgium

7

-

Switzerland

6

-

Finland

6

-

Sweden

6

-

Portugal

5

-

Poland

5

-

Austria

4

-

Norway

3

-

Bulgaria

3

-

Denmark

2

-

Slovenia

2

-

Czech Republic

2

-

Estonia

2

-

Hungary

2

-

Lithuania

2

-

Ireland

2

-

Romania

1

-

Russia

1

-

Greece

1

-

Ukraine

1

-

Luxembourg

1